Introduction

As a condition of the permission for the Northern Runway at Gatwick Airport, 54% of air passenger journeys must be

by public transport. This report, prepared by a sub group of members of CILT(UK)’s Aviation and Strategic Rail Policy Groups, discusses how this can be achieved.

Summary

With the Northern Runway in full operation, rail passengers using

Gatwick Airport Station could rise from around 19 million currently to 40 million in the 2030s and 2040s. However, because air passenger peaks do not coincide with rail peaks, there is generally spare capacity which can be made available. More capacity on weekday daytime services between Gatwick and Victoria can be provided by using rolling stock which is mostly already available but not used at off-peak times.

More air passengers can be attracted by increasing train frequencies at night and at weekends again using existing rolling stock. More air passengers will also be attracted if all Victoria services are branded as Gatwick Express and provided with enhanced customer service.

For routes other than Gatwick-Victoria and Gatwick-Thameslink, there are also opportunities to amend services to better

meet air passenger flows without reducing other routes, for example at night and on Sundays. Extending existing rail services to and from Kent should be considered, with enhanced coach services as an alternative.

The option to increase frequencies at peak times remains for the longer term. There may be opportunities for additional trains with the current infrastructure by improvements in signalling or other enhancements, but we do not see the justification for major increases through major track schemes.

While many of the options to provide increased capacity are possible at modest increased cost, the potential revenue from rail fares paid by additional air passengers is significant and should enable expenditure to be justified.

This report recommends that the DfT, GBR, Gatwick Airport and the local authorities should consider the following to enable a 54% Public Transport Mode Share to be achieved:

• Either increase the Thameslink night service to half hourly or introduce a new hourly service between Victoria and Gatwick.

• Increase the frequency of trains on Sundays.

• Devise and implement a marketing strategy for all Gatwick-Victoria services to be the same brand and the same fare.

• Investigate options for serving Kent by direct rail services.

These proposals can be implemented independently, albeit as part of an overall strategy, as and when air passenger numbers increase.

The Northern Runway

Gatwick Airport were given permission to convert the existing emergency-only Northern Runway to full use by the Secretary of State for Transport on 21 September 2025. A condition of the permission is that a Public Transport Mode Share (PTMS) of 54% is achieved before new runway can be used1. 1It is possible that this could be achieved, the runway brought into use and then subsequently the share falls. In these circumstances, it is not clear what sanction there would be. However, for this report, we have assumed that the 54% requirement continues at least until the airport’s capacity is reached. ... With the Northern Runway in full operation, rail passengers using Gatwick Airport Station could rise from around 19 million currently to 40 million in the 2030sand 2040s ...

Gatwick Air Passengers

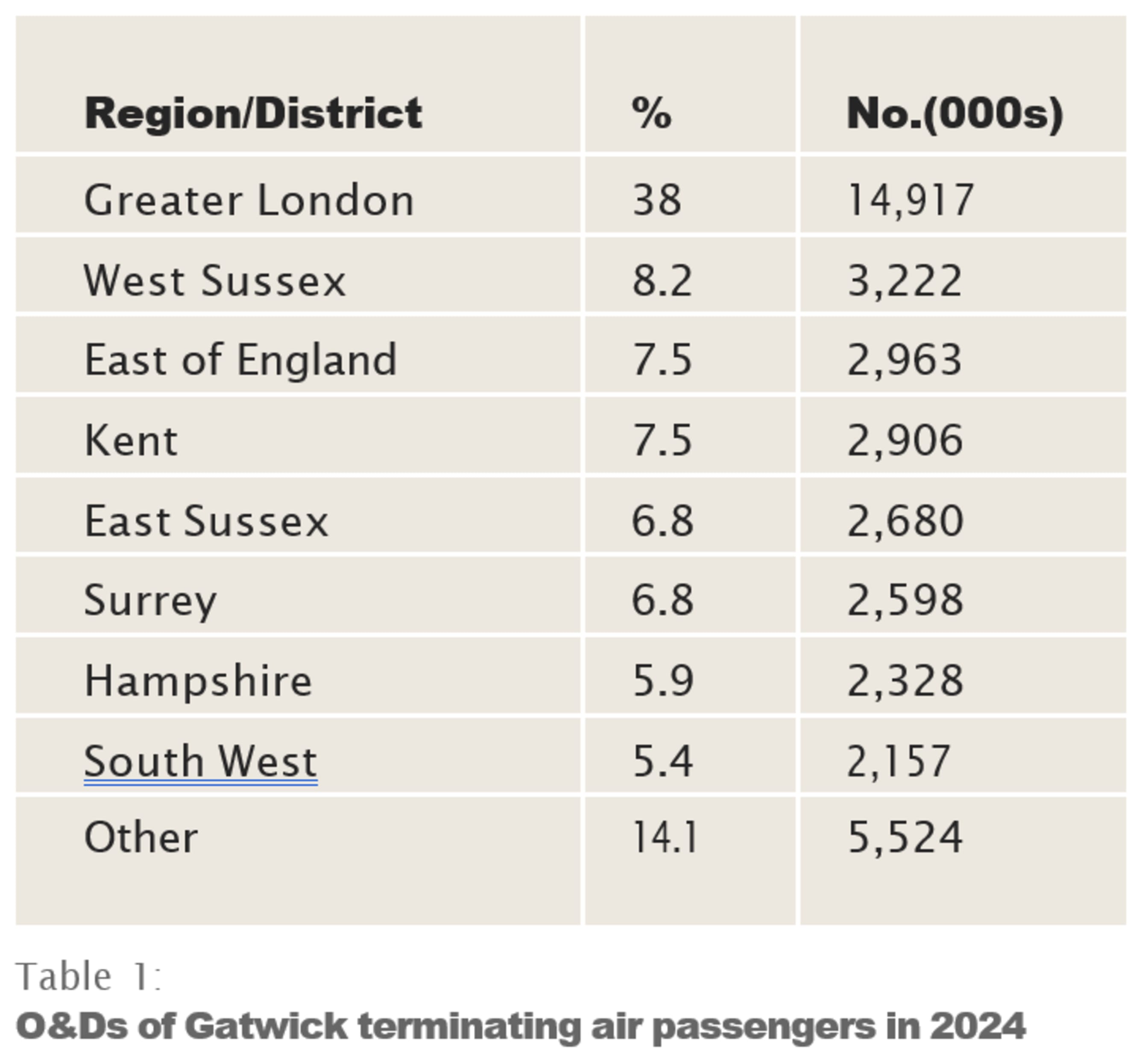

In 2024, there were 43.2 million air passengers at Gatwick of whom 40.5

million were terminating (not connecting) and therefore had a surface access journey to or from the airport. 79.1% of these were UK residents and 90.1% were travelling for leisure purposes. The main origins and destinations are set out in Table 1.

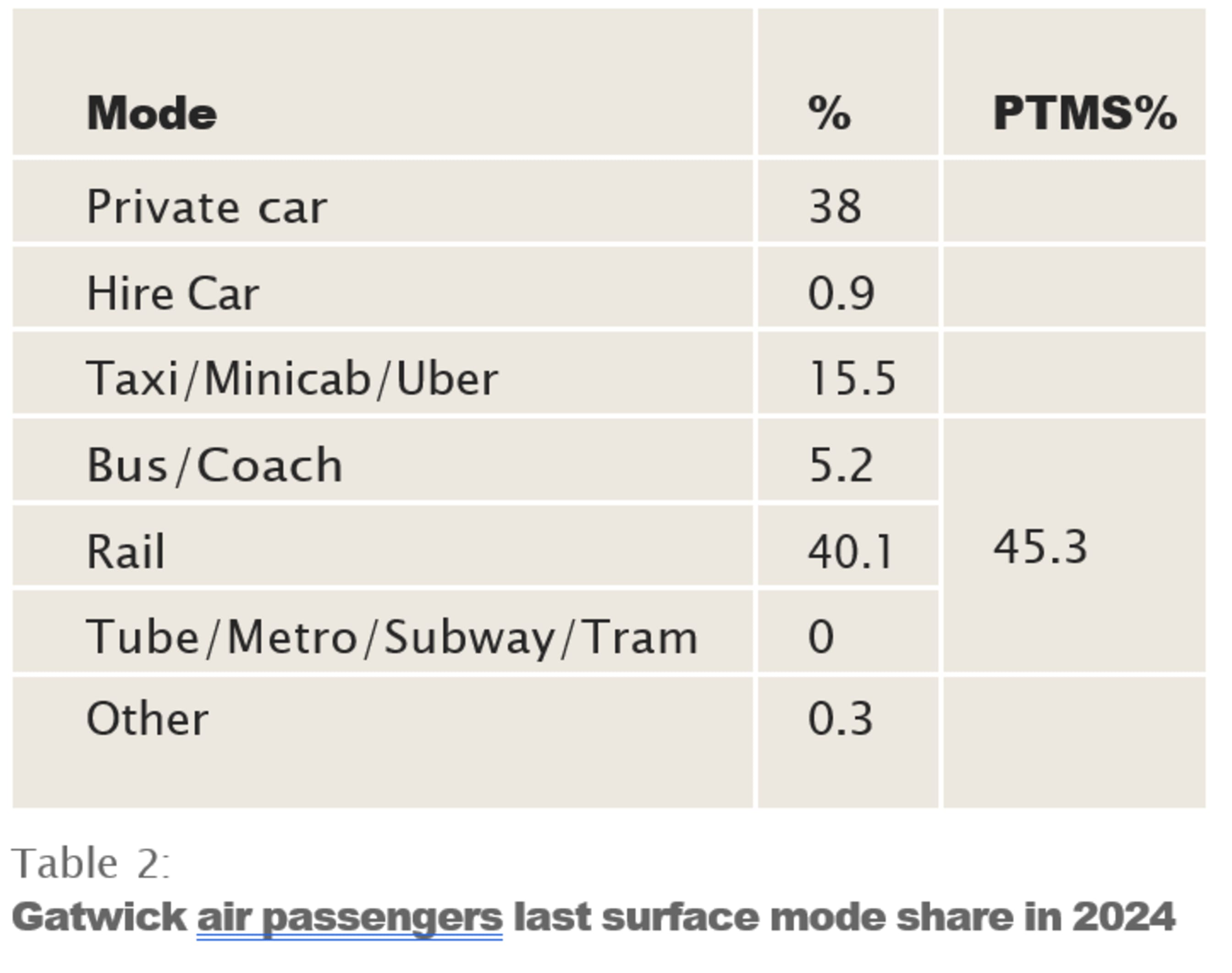

The last surface mode of air passengers is set out in Table 2. 40.1% of the terminating passenger total of 40.5 million is 16.2 million air passengers using Gatwick Station in 2024.

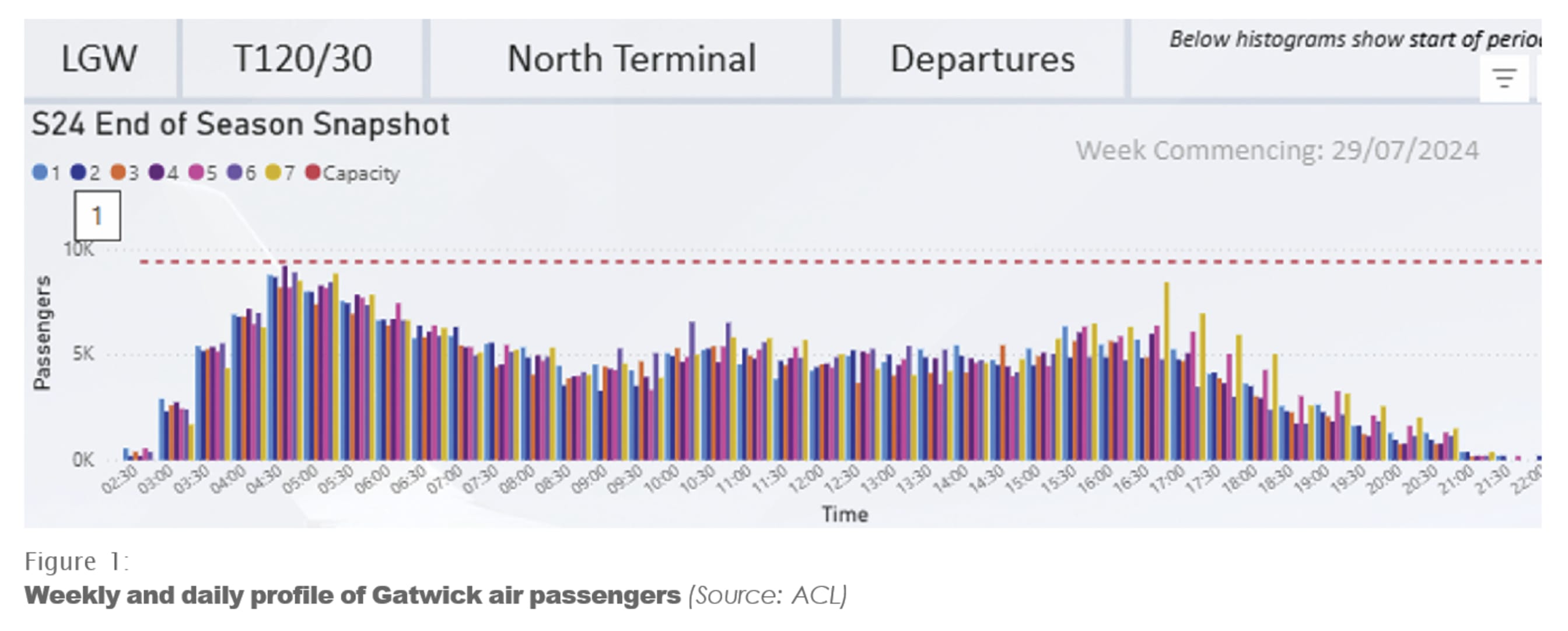

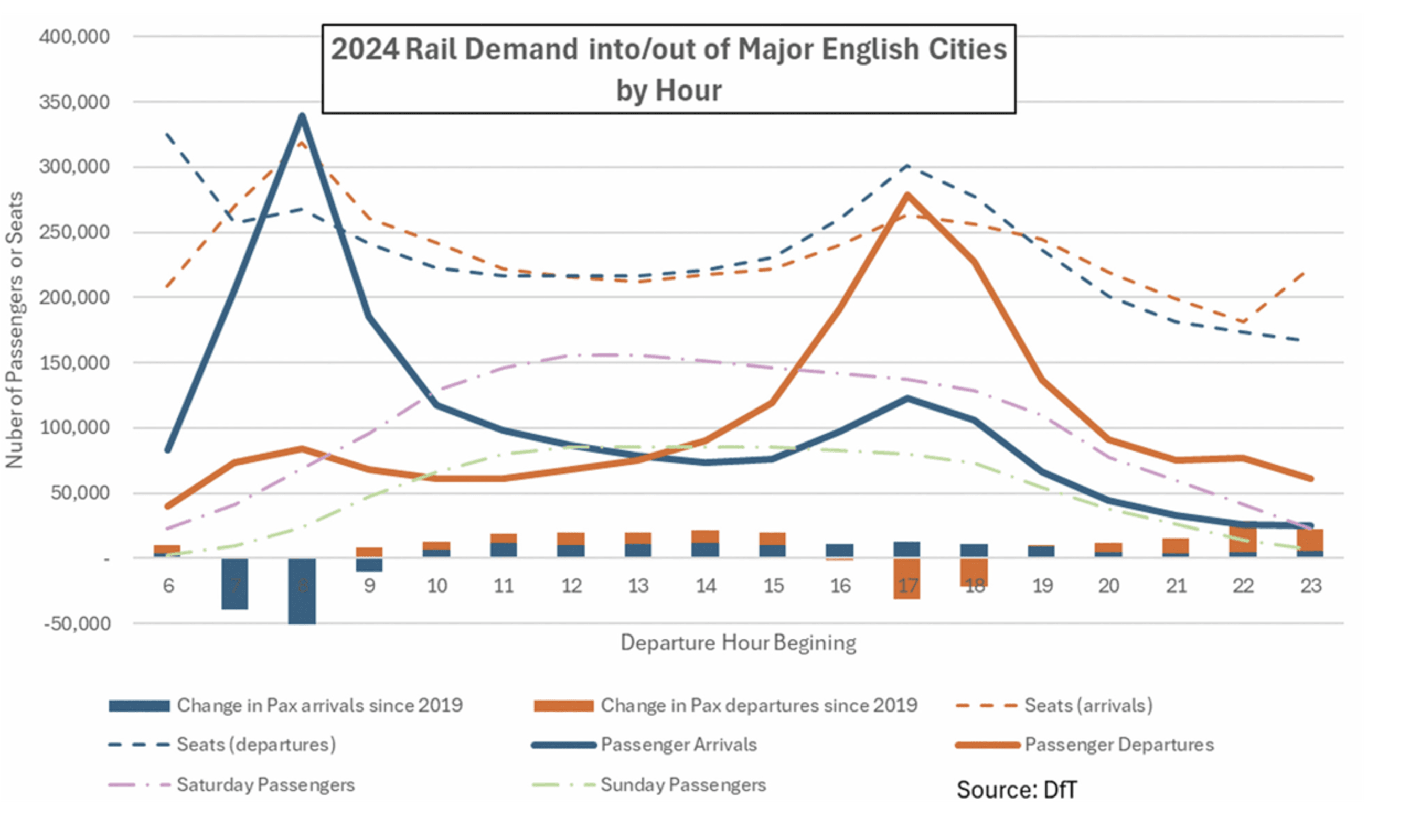

The weekly and daily profile of air passengers is as shown in Figure 1. This particular example is for departures from the North Terminal in Summer 2024. The first passengers get to the airport from 03:00 with the largest numbers at 04:30. The profile is relatively flat after the first peak. Most days

of the week are similar, but Sundays (day 7) have a distinct evening peak. The arrivals profile starts later in the morning but continues later in the evening. The South Terminal profile is different with a later morning peak at 08:30. Both terminals together provide a relatively flat profile throughout the day.

... Extending existing rail services to and from Kent should be considered, with enhanced coach services as an alternative ...

Gatwick Rail Passengers

In 2023/24 there were 19.5 million entries/exits from Gatwick Station with

O&Ds as in Table 3. The difference between

19.5 million rail passengers and 16.2 million air passengers using rail is non air passengers using Gatwick Airport Station.

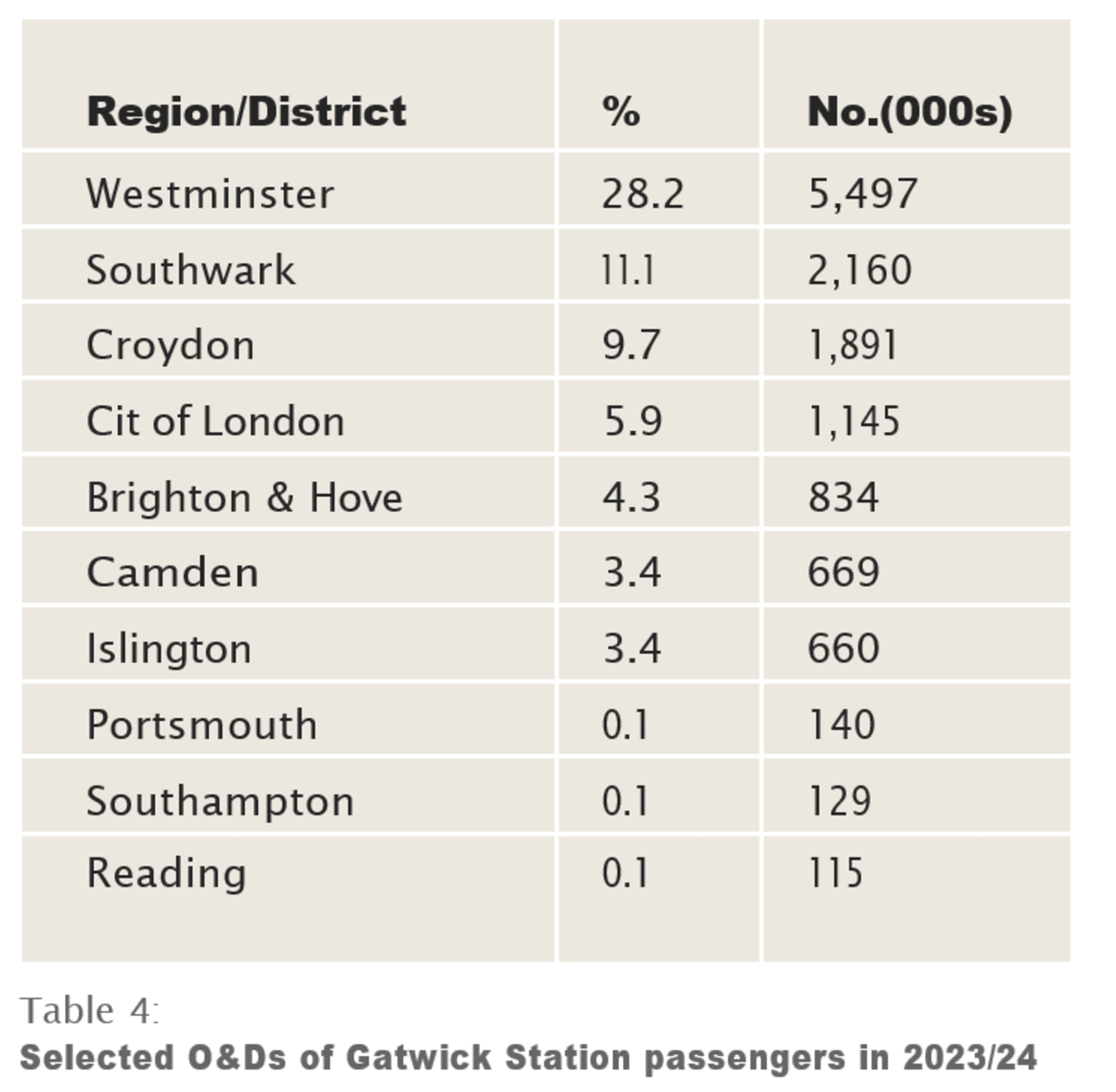

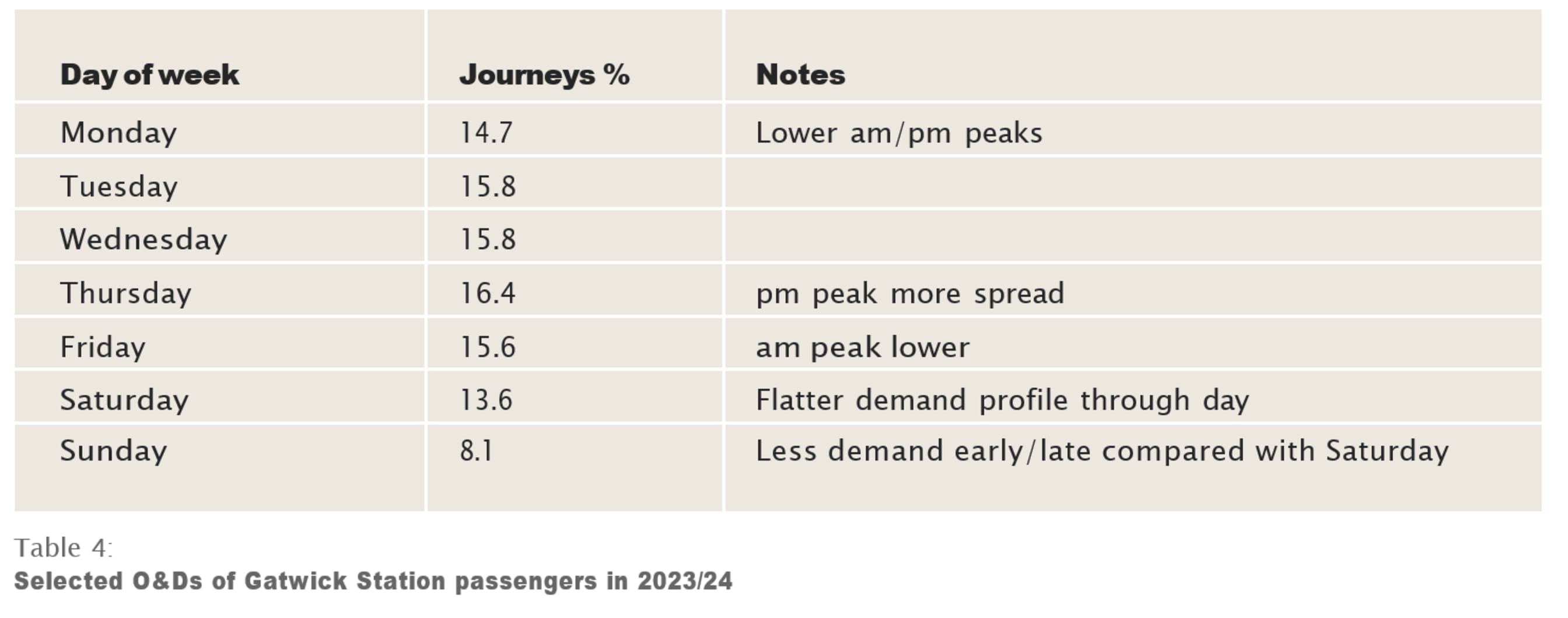

More detail of some O&Ds by districts is shown in Table 4.

Table 5 shows a typical rail profile by day of week and Figure 2 shows a typical rail profile by time of day. In Table 5 the reduced lower number of journeys on Sundays may reflect the lower number of services available as well as lower demand. In Figure 2 note that peak demand has reduced since 2019.

Comparison Between Air and Rail Passengers

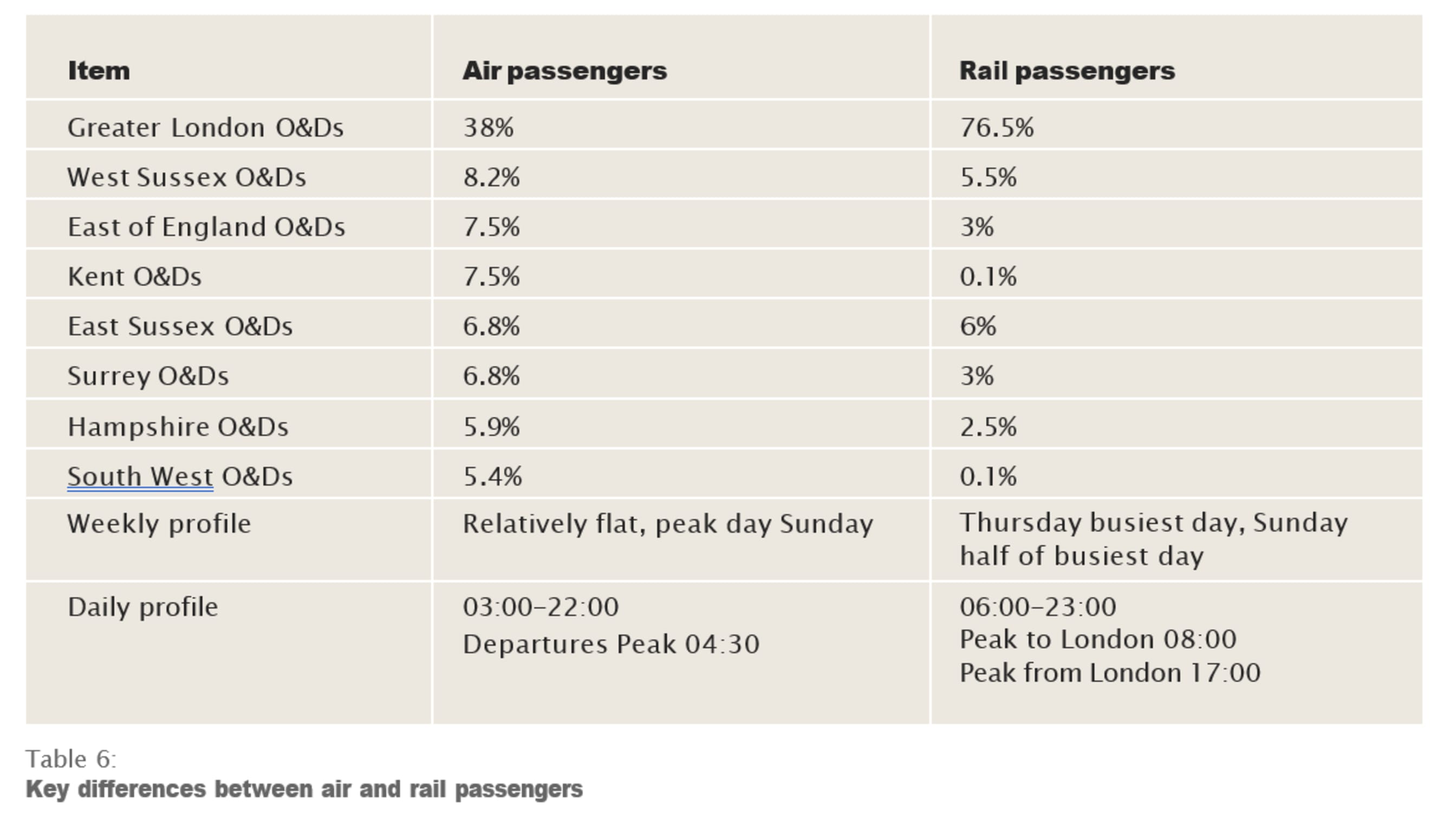

Table 6 shows some key differences between air and rail passengers. Clearly

rail is used by a large proportion of London O&D passengers, but the coverage of direct rail services is extensive, especially when compared with other UK airports.

Regions with significant O&Ds but few rail passengers are Kent and the South West, where there are no or few direct services. In terms of weekly and daily profiles, air passengers are less peaky in terms of day of the week and time of day.

Gatwick Rail Services

The current pattern of northbound rail services in the standard weekday off peak

hour commencing 1100 through Gatwick Station is set out in Table 7. In summary, this is 6 Southern to Victoria, 2 Gatwick Express to Victoria, 8 Thameslink to London Bridge and 2 GWR to Reading. All the Southern, Gatwick Express and 4 Thameslink are on the Fast Lines, and 4 Thameslink and 2 GWR are on the Slow Lines (although this increases to

12 at Redhill where Reading and Tonbirdge services reverse). Total 18 trains per hour. There are additional trains in the peak hours. The Sunday service is 4 Southern, 2 Gatwick Express, 6 Thameslink and 2 GWR, total 14 trains per hour. There are also freight, operational and maintenance movements.

Between 2019 and 2025, the number of trains at Gatwick Airport per day has declined from 855 to 821. The largest single reduction is

the dropping of 2 Gatwick Express trains per hour. However, there have been increases

in freight trains.

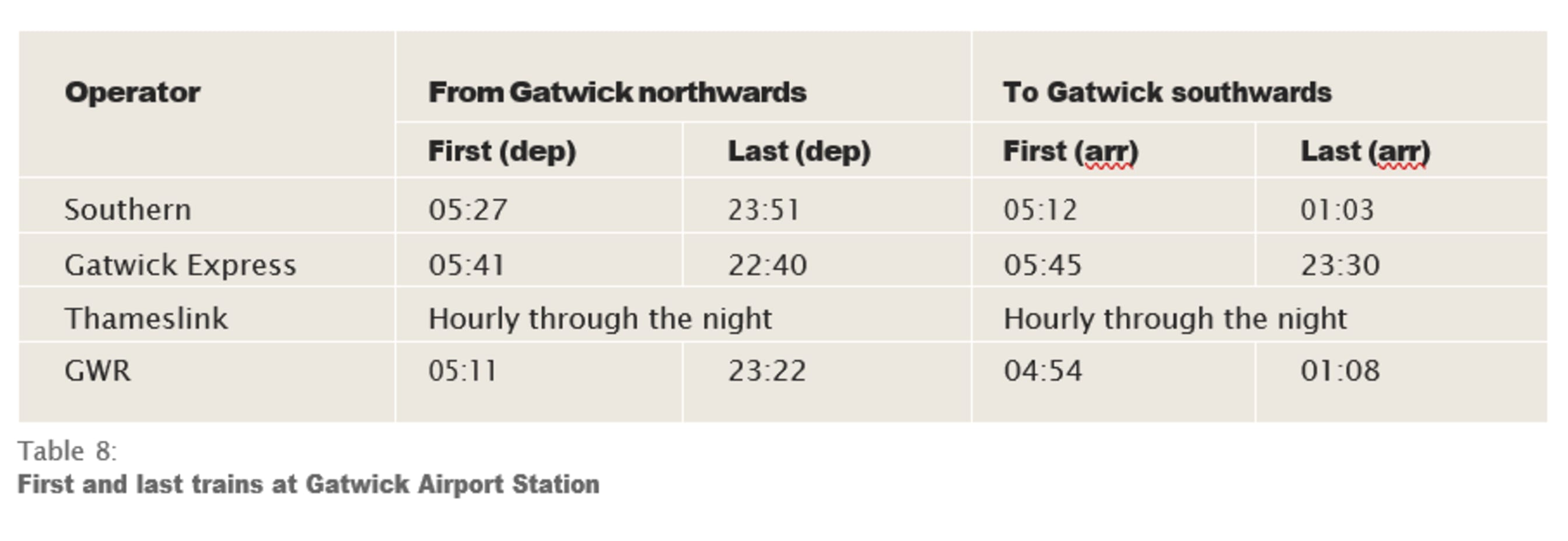

The first and last trains are set out in Table 8.

The Southern trains are 12 carriages in the peak, 8 cars off peak. Gatwick Express is 8 carriages, Thameslink is 12 carriages and GWR is three carriages. South of Gatwick the Southern Horsham trains from Victoria divide at Horsham for Portsmouth Harbour and Bognor Regis partly to meet demand and partly because of limited power supplies

and short platforms.

...Between 2019 and 2025, the number of trains at Gatwick Airport per day has declined from 855 to 821...

Future Demand

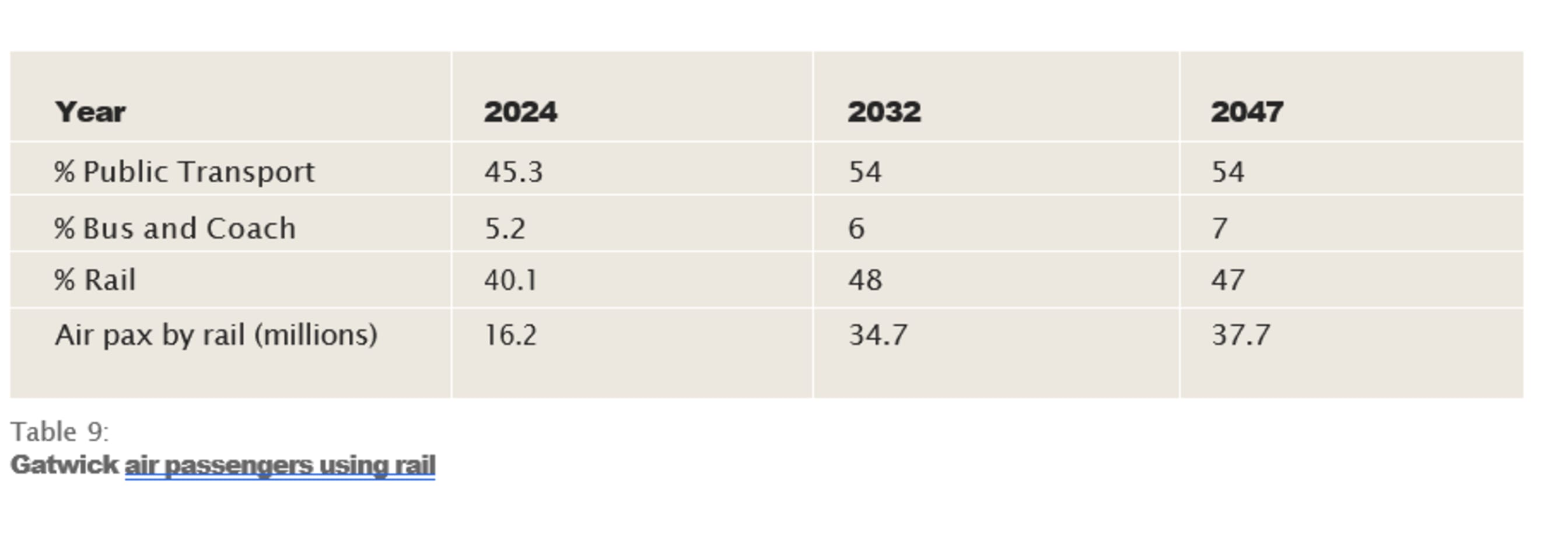

Various figures have been used for the growth of passengers with and without the Northern Runway. The Environmental Assessment included a forecast of 72.3 mppa (millions of passengers per annum) for 2032 and 80.2 mppa for 2047 with the project, compared with 59.4 and 67.2 mppa without the project. Whilst it is appropriate to use highest case figures in an environmental assessment, it is CILT(UK)’s view that these figures are optimistic and our 2024 report on a new ANPS suggested that Gatwick would have between 52 and 58 mppa in 2035.

With the target of a 54% PTMS and making an assumption that the bus and coach share would be 6% and 7% in 2032 and 2047 respectively, the rail share of the Environmental Statement forecasts would be as shown in Table 9. This is a large potential market and, making a crude assumption of an average fare of £10 per journey, the additional revenue could be around £200 million per year.

It is possible that the characteristics of these future air passengers could be different from the existing as set out in the paragraphs above, for example in terms of terminating, O&Ds, or time profiles. With additional runway and terminal capacity, it would be possible for peaks to grow as well as some peak spreading and, for this report, we have assumed similar characteristics to the existing.

Non air passengers are also expected to grow, possibly by around 2.5% pa. This would result in the number of non air passengers using Gatwick Station rising to about 4 million in 2032 and 6 million in 2047. This would give total rail passenger numbers at Gatwick Station of around 39 million in 2032 and 43 million in 2047. Additionally, domestic demand passing through the station, from south to north of Gatwick Airport, may grow from around 19 million today to around 34 million by 2047. These passengers will be sharing the same tracks and usually the same trains as airport passengers, adding to the route’s long-term capacity requirements.

Accommodating Additional Rail Passengers

The success of any enhancement option will depend on the ability to attract air passengers from other modes, which is determined by perceptions of the following, which we use in determining which of the options should be pursued:

Journey time: On routes to and from most of London, rail will tend to be the quickest route. For journeys outside Greater London, some journey times are quicker by road.

Reliability: Rail has a (probably undeserved) reputation for unreliability whereas road journeys are perceived (probably wrongly) to be in the control of the driver. Departing air passengers are particularly concerned to ensure that they do not miss their flight

Cost of travel: Rail is perceived as expensive, especially for families, compared with the fuel cost of car. Car parking is a significant element of car journey cost but is not always perceived as part of the journey cost.

Taxi fares are a more accurate indicator of cost. Coach fares tend to be considered good value for money

Comfort: As well as basic comfort, which is often seen as superior in a car or taxi, there is the ease of carrying baggage.

Interchange: A significant disincentive for any journey, it is especially important for air passengers because of issues such as reliability and baggage carrying.

Marketing: Air passenger journeys are made infrequently compared to other rail journeys, so air passengers may not be familiar with the network, the timetable, the fares or other aspects of the journey, whereas a taxi or car will remove these concerns. A marketing strategy which targets air passengers will attract air passengers.

In the following paragraphs the following options are considered:

• Additional carriages on existing services

• Additional services (peak and off peak)

• Marketing (including branding, fares and customer service)

• Additional station capacity

• Additional infrastructure

• Bus and Coach

Additional Carriages on Existing Services

It is clear from the hourly profiles that air and rail peaks do not coincide. The morning departing air passenger peak is 2-3 hours before the rail peak and in the opposite direction (southbound). The morning arrivals air passenger peak (northbound) is after the rail peak which drops by about two thirds after 09:00. The evening air passenger peaks are generally less and the evening southbound rail peak at 17:00 does not coincide with an air passenger peak.

Currently, Southern trains are 12 carriages in the peak, 8 cars off peak. Gatwick Express is 8 carriages, Thameslink is 12 carriages and GWR is three carriages. Extending the times when Southern Trains are 12 carriages and adding more carriages to Gatwick Express trains would give a capacity increase of 50% for the 8 Southern plus Gatwick Express services, or a 33% increase in capacity on the Fast lines. This would require the acquisition of additional rolling stock and, as currently at peak times, some of these 12 carriage services would have to split and join south of Gatwick.

Many of these additional carriages are clearly available already, so there would be a modest cost in increased electricity usage. Some new rolling stock might need to be acquired, although the Electrostar fleet is very large (around 220 four car units on Southern and Gatwick Express) and mostly interchangeable. Interior layouts vary from 2+2 with baggage racks for Gatwick Express to 3+2 on some Southern variants. It is also appreciated that more intensive use at off peak times will impact on maintenance schedules which might also lead to a need to acquire more rolling stock. The detail of how additional carriages could be implemented on each route can be considered in relation to refurbishment, cascading, acquisition and other ongoing programmes and can be phased as growth occurs.

The additional carriages would provide more capacity on the key Gatwick-Victoria route. The data clearly indicates that London and, in particular, Westminster, are the largest O&Ds, being the tourist and commercial centres.

This route also serves Croydon, also a large O&D, and interchange opportunities at Clapham. Given that this additional capacity would be provided in the rail off peak, there should be plenty of capacity at the stations. No additional capacity would be provided on the Thameslink route although this already has significant spare capacity off peak.

Additional Services

The current total of 12 timetabled trains per hour on the Fast lines and 6 trains per hour on the Slow lines (12 per hour at Redhill) in the standard hour is less than the theoretical capacity which would be 17 trains per hour on each line with 3.5 minute headways. A practical capacity would be 12 trains per hour on each line which would leave 5 paths for freight and non-timetabled trains and recovery time on the Fast lines.

At peak times more trains are timetabled with less provision for other trains. All lines are therefore practically at capacity in the standard hour.

Considering the hourly and daily profiles of air passengers, there are times of the day and week when air passenger demand is high but rail services are limited. Air passenger demand is apparent through the night, in particular from about 0300 and is served only by an hourly Thameslink service. Similarly, last trains northwards may be after the last flight arrivals. There would appear to be an opportunity to add an hourly service to and from Victoria throughout the night, or perhaps an earlier start and later finish to the Southern and Gatwick Express services, or make the Thameslink service every half hour. Given the large number of O&Ds in Greater London, the enhancement which achieves greater mode switch would depend on a more detailed consideration of O&Ds by borough. It is understood that GWR are planning to introduce a night service to Gatwick and this should be a good trial to see if these longer distance routes are successful, noting the proportionately lower rail O&Ds from Surrey, Hampshire and the South West. It should not be forgotten that air passengers have to get to or from a station and this may be by car or taxi or on some routes, by Night Tube. With roads usually quieter at night, car or taxi (or coach) may seem more attractive for the whole journey but there is nevertheless an opportunity to serve air passengers at night.

Another opportunity to serve air passengers is on Sundays, when the rail service reduces by 4 trains per hour but when air passenger demand is very close to the highest of any day. Again the rolling stock is available and there would in addition be the staff costs of running the extra trains.

There is currently an hourly service from Watford Junction to East Croydon which could be extended to Gatwick giving direct links to north west and west London as well as connections to the West Coast and London Overground. However, it would use the

Slow lines and would be a long journey, so passengers would mostly prefer to change at Clapham Junction. Another additional service that is proposed is an open access service between Newcastle and Brighton. Although infrequent and relatively slow, this would enable some routes with O&Ds north of London to access Gatwick without going through London. However, it is not yet approved and may mean that other enhancements are not possible.

In terms of new routes, Kent has the fourth largest air passenger O&Ds. The current hourly service between Tonbridge and Redhill could probably be extended to Gatwick with some modifications required to platforms and signals at Redhill, and there would be capacity on the Slow Lines. It could also be extended further into Kent to serve the larger communities such as Canterbury and Ashford, but the attractiveness of a direct service will depend on whether it is better than the frequent services via London, which require a change, or indeed better than the road journey.

For passengers from Hampshire, it is also worth noting that the hourly Southampton to London Victoria service via Horsham and Gatwick Airport was removed in June 2024 to facilitate capacity and performance improvements elsewhere across the south coast. Passengers originating in Southampton now have to change at Barnham, but looking at how to reinstate direct services in the years ahead may help increase the rail market share.

Night and weekends are often used for infrastructure maintenance as traditionally this is a quieter time for rail passengers.

The Brighton Main Line is four track north of Three Bridges and so it is possible to keep two tracks running while maintaining the other two. This already happens on the section from Gatwick to East Croydon to accommodate the hourly Thameslink service and should be possible for all but major tasks such that additional services can be operated at night.

Marketing

(Including branding, fares and customer service)

Air passengers are generally not frequent travellers and may not be familiar with the rail network, timetable or language. A dedicated service which became the Gatwick Express was first operated in 1958 to attract air passengers and also to segregate them from commuters, who had different requirements. Over many years it has been the case that a dedicated airport express service attracts more air passengers than can be explained by comparisons of journey time, frequency, cost etc. and a specific factor (the modal constant) is used in modelling to predict ridership. The logic of this is that air passengers need the reassurance that the train is suited to their requirements and does not require any additional knowledge of the other factors. The models also demonstrate that air passengers are prepared to pay a premium fare for this service. As well as Gatwick, dedicated airport express services exist at Heathrow, Stansted, Oslo, Stockholm, Hong Kong, Kuala Lumpur and other cities.

The differential between the Gatwick Express and Southern services is now small. The journey time is 30 minutes for Gatwick Express compared with 32 on Southern, and the frequency is now 2 per hour compared with 6 Southern. These two trains operate non stop from Victoria to Gatwick but then continue to Brighton, with an intermediate stop. They operate from dedicated platforms at Victoria and, while there used to be a train always waiting on the Gatwick Station platform, this is no longer the case. The trains have 2+2 seating with baggage racks and the Gatwick Express branding is clearly aimed at air passengers with a dedicated website and specific advertising campaigns plus multilingual signing and announcements.

The rolling stock now used on Southern trains are more comfortable and reliable than their predecessors. The standard single peak fare is £24.10 on Gatwick Express compared with £21.30 on Southern although there are many variations. Compared with earlier times, the Gatwick Express service has been altered to serve more than just the air passenger market, thus introducing some compromises in the internal layout and frequency.

The options for the Gatwick-Victoria service are:

• Option 1: Retain the existing branding and service (2 Gatwick Express plus 6 Southern)

• Option 2: Retain the existing branding and amend the service (4 Gatwick Express and 4 Southern)

• Option 3: Brand all eight as Southern

• Option 4: Brand all eight as Gatwick Express

Option 1 is unsatisfactory as it retains the Gatwick Express branding for a service which is less than premium. The fare differential causes confusion, reduces optimal capacity use and is difficult to justify.

Option 2 could provide a more premium service but, if the East Croydon and Clapham Junction stops are removed, this will lead to inconvenience for passengers wishing to travel to/from these stations, and for other parts of south London.

Option 3 would be straightforward and would give the most flexibility, but would not attract as many air passengers as there would be no dedicated branding.

Option 4 would provide a high frequency between Gatwick and Victoria without a distinction between fares and, provided it is done carefully, could be marketed as a Gatwick Express service, albeit with some trains calling at East Croydon and Clapham Junction.

This branding could perhaps be more subtle than currently so as not to exclude non air passengers. This is similar to the Stansted Express which calls at intermediate stations with less overt marketing, which is also the case on the Luton Express. It could be achieved gradually over several years with changes to rolling stock and a freeze on Gatwick Express fares until caught up by Southern.

In addition to the fare differential between Gatwick Express and Southern services between Gatwick and Victoria, there is a much larger fare differential between Southern services and Thameslink, the fare to Blackfriars, Farringdon and St Pancras being £15.10. This is a long standing difference and should be removed, albeit gradually by freezing the higher fares and allowing the lower fares to grow over time. Other fares are also complex such as returns or counter peak, and contactless ticketing means that fares may not be known until the passenger taps in (and even then not noticed). Fares reform is seen as important over the whole rail network and has started in places but is mired in complexity and difficult to change.

Nevertheless, a long term objective should be that there is no difference between Gatwick and central London fares. For air passengers, who may be foreign or less frequent travellers, the key should be simplicity, so that they are not put off by a complex array of fares with different conditions.

Rail fares are considered by passengers in comparison with the costs of other modes. Taxi is usually more expensive than rail for one person, but two or more passengers may make the total cost more comparable. Taxi fares include the drop-off or a short stay car park charge. Private car costs are rarely perceived in full, even if the fuel cost is counted, but drop off and parking charges may be significant, especially for long stay parking. Drop off and car parking fees are in the direct control of the airport and can be changed to affect the differential but they are an important source of revenue which the airport will be reluctant to risk. The drop off fee is to be increased significantly in 2026, partly to increase the difference between ‘carrot and stick’. Coach fares are usually cheaper than rail and this may be a particular issue in attracting air passengers on some of the longer routes, such as to the South West. The overall cost of access may be perceived as small as a proportion of the total trip cost (including air fare and accommodation).

As already noted, air passengers require reassurance that they will catch their flight, or that they are on the right train to get to their destination. The most effective way to provide this is through the existing information systems, supplemented by people, on the train, at the stations and elsewhere. On the train, conductors, revenue inspectors, or whatever they are called, are capable of providing such reassurance, as well as safety and revenue duties. Similar safety and information roles can be done by platform staff. Ticket offices are in decline as more passengers use smart cards or devices, but customer information at several locations is very productive in enabling air passengers to choose rail. Mobile sales and information staff can direct and persuade potential passengers and should be incentivised to do so.

Additional Station Capacity

It was noted earlier that, because air passenger peaks do not coincide with rail peaks, there would be capacity at stations to accommodate growth in air passengers, although station dwell times may also need to be reviewed as the proportion of passengers with luggage increases, and reflecting that they may be joining already busy trains. The exception to this is Gatwick Airport Station itself, where the majority of rail passengers are air passengers. Significant improvements have taken place at Gatwick Station in recent years, including the provision of an additional platform, lifts and escalators and a new concourse for rail arrivals.

The ‘old’ concourse is now used by rail departures only and has plenty of space for current users. The current layout can be adapted as more passengers choose pay-as-you-go or mobile ticketing and there should be enough space to accommodate the growth. The platforms are also all sufficient to accommodate 12 car trains but structures on the platforms inhibit movement and cause crowding.

Better management combined with some rearrangement of these structures (eg. canopies on open sections) should enable passengers on longer trains to be accommodated.

Additional Infrastructure

As it appears that lengthening trains and adding services at off peak times will be sufficient to accommodate additional air passengers, there is no need for major infrastructure improvements for additional Gatwick passengers. The Croydon Area Remodelling Scheme was being developed in the pre-Covid years to provide additional peak capacity but, with the reductions in rail peak passengers, this is now impossible to justify.

There may be other infrastructure improvements such as signalling which can enhance reliability or resilience and these should of course be pursued when justified.

...The Croydon Area Remodelling Scheme was being developed in the pre-Covid years to provide additional peak capacity...

Bus and Coach

Although this report is about rail access, bus and coach is currently used 5.2% of air passenger trips and can be expected to accommodate many more as the airport grows. Other London airports have higher bus and coach shares and, while coach is not very attractive for Gatwick-central London journeys, many other places are not well served by rail, and coach could be an attractive alternative to car and taxi.

Coach operators are able to start operations quickly and can adapt their services, filling in gaps and operating when there is demand. As with rail, coach services marketed for air passengers are particularly attractive. Kent is an example of a significant O&D for air passengers where there is no direct rail service and, for North Kent, not much chance of there being one, where a coach-airport service could attract a significant share of the market. However, previous attempts at such services have not been successful.

We have not considered staff journeys in looking at rail access, although undoubtedly some staff use rail. There is no condition on mode share for staff although targets are included in the Airport Surface Access Strategy to reduce single occupancy car and increase public and active transport. Local buses are the most significant element of public transport for staff.

Conclusion and Recommendations

With the Northern Runway in full operation, rail passengers using Gatwick Airport Station could rise from around 19 million currently to 40 million in the 2030s and 2040s. However, because air passenger peaks do not coincide with rail peaks, there is generally spare capacity which can be made available. More capacity on weekday daytime services between Gatwick and Victoria can be provided by using rolling stock which is mostly already available but not used at off-peak times. More air passengers can be attracted by increasing train frequencies at night and at weekends again using existing rolling stock. More air passengers will also be attracted if all Victoria services are branded as Gatwick Express and provided with enhanced customer service.

The requirement is to achieve a 54% public transport share by the opening of the Northern Runway around 2030, and we consider that there would be sufficient rail capacity to achieve this, in part because we think that the number of passengers will not be as high as used in the Environmental Statement. The various options noted above can be implemented in a phased programme as the number of passengers grows and also as the rolling stock is refurbished and, in the longer term, replaced. Some can be implemented early such as additional trains at night and on Sundays.

For routes other than Gatwick-Victoria and Gatwick-Thameslink, there are also opportunities to amend services to better meet air passenger flows without reducing other routes, for example at night and on Sundays. Extending existing rail services to and from Kent should be considered, with enhanced coach services as an alternative.

The option to increase frequencies at peak times remains for the longer term. There may be opportunities for additional trains with the current infrastructure by improvements in signalling or other enhancements, but we do not see the justification for major increases through major track schemes.

While many of the options to provide increased capacity are possible at modest increased cost, the potential revenue from rail fares paid by additional air passengers is significant and should enable expenditure to be justified.

This report recommends that the DfT, GBR, Gatwick Airport and the local authorities should consider the following to enable a 54% Public Transport Mode Share to be achieved:

• Either increase the Thameslink night service to half hourly or introduce a new hourly service between Victoria and Gatwick.

• Increase the frequency of trains on Sundays.

• Devise and implement a marketing strategy for all Gatwick-Victoria services to be the same brand and the same fare.

• Investigate options for serving Kent by direct rail services.

These proposals can be implemented independently, albeit as part of an overall strategy, as and when air passenger numbers increase.

Next Steps

We plan to engage with national government and local authorities, but we are always interested to hear from or about other interested parties, so if you have any comments on what you have read, please contact the Aviation & Strategic Rail Policy Group:

Daniel Parker-Klein

The Chartered Institute of Logistics and Transport Earlstrees Court, Earlstrees Road

Corby, Northants NN17 4AX United Kingdom