ANPS and MBU Review

Aviation Policy Group

Introduction

The Government is carrying out a review of the 2018 Airports National Policy Statement (ANPS) which gave policy support for a third runway at Heathrow. A draft revised ANPS is expected to be published in July 2026. This review sets out CILT(UK)’s views on what the draft ANPS should cover.

CILT(UK) published a report on the ANPS in August 2024 which proposed that the ANPS should be reviewed together with the Making Best Use (MBU) policy document also published in 2018. The MBU policy covers all airports in the UK other than Heathrow. CILT(UK) has also contributed to the debate through other reports, consultation responses, webinars and in media, key ones to note being:

April 2026: Airport Surface Access report (draft)

March 2026: Gatwick Rail Access report

February 2026: South East Airports Update webinar

February 2026: Focus magazine articles ‘Navigating turbulence’, ‘Air cargo’s hidden dependency’, and ‘Wings of change’

October 2025: Response to Environmental Audit Committee report on airport expansion and climate targets

November 2025: Manchester Airport and Wider Airports Policy webinar

February 2025: Stansted Sustainable Development Plan response

January 2025: CILT(UK) welcomes Heathrow expansion announcement press release

January 2025: Bristol Airport Draft Master Plan consultation response

August 2024: Airports National Policy Statement report

March 2024: Airport Surface Access report

February 2024: Gatwick Northern Runway written statement to inquiry

August 2023: Luton Airport Expansion written response to inquiry

August 2022: Air freight briefing paper

May 2022: Airport expansion report

CILT(UK) was invited to a stakeholder roundtable on 28 February 2026 related to air cargo and contributed insights to the DfT review team.

Executive Summary

The ANPS review should cover the whole of the UK and should therefore incorporate the MBU policy.

The expansion at any airport should be permitted if there is a positive balance of benefits and costs – provided the airport is prepared to invest in expansion.

While DfT’s aviation forecasts can be a starting point, the revised ANPS should consider scenarios where the need for expansion at individual airports depends on the individual merits of each case.

There is sufficient existing and potential capacity within the UK, and particularly within the South East and East of England, without a third runway at Heathrow for the next twenty years.

However, CILT(UK) would support expansion at Heathrow including a third runway if a case can made that the benefits - including the benefits of a hub operation and increased competition – outweigh the costs (including local environmental costs and the appropriate contribution to surface access) and that the airlines can agree an acceptable funding arrangement, and as such expansion should be safeguarded.

Changes in aircraft size will, on the one hand, continue to result in an increase in average loads – making better use of existing runway capacity. On the other hand, new long haul aircraft types will enable thinner routes to be operated directly without the need to fly via a hub.

The revised ANPS/MBU must include an analysis of and forecast for air cargo, including the role of integrators, trucked air cargo and forecasts, noting the specific requirements of all-cargo aircraft operations.

Surface access may constrain expansion at some airports unless funding solutions are found for infrastructure.

The Climate Change Committee’s advice on aviation expansion should demonstrate how the 2050 net zero commitment will be met.

The ANPS and MBU

The ANPS was ‘designated’ (approved by Parliament) in June 2018 following the report of the Airports Commission in 2015 and significant scrutiny and legal challenge. At the same time, the MBU was published, following a consultation.

The ANPS has five sections, as follows:

Introduction

The need for additional airport capacity

The Government’s preferred scheme:

Heathrow Northwest Runway

Assessment Principles

Assessment of Impacts

CILT(UK)’s expertise and insight should assist in reviewing the need and in considering the assessment principles and impacts in the areas of air cargo and surface access, so this note focuses on these areas.

The MBU (full title ‘The future of UK aviation: Making best use of existing runways’) is a relatively short document noting the general principle of support and requiring proposals to be judged by the relevant planning authority based on economic and environment impacts and mitigations, each case being considered on its merits.

CILT(UK)’s clear view is that the revised ANPS should incorporate the MBU policy so that it is properly a National policy statement.

...While DfT's aviation forecasts can be a starting point, the revised ANPS should consider scenarios where the need for expansion at individual airports depends on the individual merits of each case...

The need for additional airport capacity

The ANPS relies on the Airport Commission’s analysis of demand and

capacity which began with considering DfT’s aviation forecasts, but which developed forecasts of their own. They were based on activity in the early 2010s. Figure 1 shows total UK passengers and shows that passenger numbers fell dramatically during the period 2020 to 2022 and recovered to about 300 million in 2025.

The 2025 actual is not dissimilar to the Airport’s Commission’s national forecast for that year, and neither is the 2017 DfT forecast (Low 280m, Central, 295m, High 310m).

However, the key difference from the Airports Commission’s report is that they focused on the South East and looked at individual airports, concluding in their Interim Report that, without additional capacity, they would be full as follows:

Heathrow 2010

Gatwick 2020

London City 2024

Luton 2030

Stansted 2041

...It is not clear why the Airports Commission concluded that Heathrow had been full from 2010 when it handled 65.7 million passengers on 449,000 ATMs. In the years beyond 2010, growth was to 80.9 million passengers and 476,000 ATMs in 2019...

It is not clear why the Airports Commission concluded that Heathrow had been full from 2010 when it handled 65.7 million passengers on 449,000 ATMs. In the years beyond 2010, growth was to 80.9 million passengers and 476,000 ATMs in 2019.

The most recent DfT assumptions on airport capacity were included in the Jet Zero modelling in 2022, which for 2019, for airports in the South East and East of England were as follows:

Heathrow 480,000 ATMs

Gatwick 291,000 ATMs

London City 111,000 ATMs and 6.5 million passengers

Luton 160,000 ATMs and 18 million passengers

Stansted 259,000 ATMs and 35 million passengers

The modelling assumed that these capacities would increase in future years but the first year modelled was 2030.

In the last few years, approval has been given for several expansions which means that the near future capacities will be, and will continue to grow, as follows:

Gatwick with a Northern Runway increasing to around 75 million passengers by the late 2030s such that it can continue to grow relatively unconstrained.

London City up to 9 million passengers, which is more than twice its 2025 throughput, although demand will be constrained by the continuing weekend limits.

Luton 32 million passengers as the second terminal begins operations, with some spare capacity before then in the next few years.

Stansted 259,000 ATMs and 51 million passengers, providing significant room for passenger growth, albeit depending on increasing average loads.

If smaller airports are included (Southend, Southampton, Manston, Norwich), there is further scope for growth.

Although no approval has been given for expansion, Heathrow’s capacity of 480,000 ATMs can continue to accommodate more passengers with increasing average loads to about 92 million.

Outside the South East and Eastern regions, there are few capacity constraints and therefore there is scope for growth if demand can be attracted. Airports worth noting are as follows:

Birmingham has scope for growth and HS2, due for completion in the early 2030s, will bring the airport under an hour from London.

The Northern region has plenty of sparecapacity, and there is more potential with the possible reopening of Doncaster Sheffield, if airlines can be attracted. Leeds Bradford, while currently growing, may find its longer-term growth constrained unless it can provide improved surface access. Some airports have plenty of spare capacity but limited demand although this could be stimulated by North Sea activity or green energy developments in the North East.

Manchester has significant potential which is now being demonstrated with its terminal developments. Implementation of the Northern Powerhouse Rail schemes should overcome any surface access constraint.

Northern Ireland’s airports serve their specific market but have ambitions to grow significantly

Scotland’s airports can grow to meet its demand, with surface access needing improvement at Glasgow and Aberdeen.

Bristol Airport may be constrained if it does not obtain approval to expand, for example because of surface access issues, and the other airports in the region, and in Wales, find it difficult to compete. Bournemouth Airport may grow if it can attract some South East passengers.

Cargo capacities are considered separately below.

It is anticipated that new DfT forecasts will be included in the draft revised ANPS, and these are important in terms of demonstrating the GHG emissions at national level (see section below on GHG Emissions). However, previous versions of the allocation element of the DfT forecasting model result in demand being allocated first to the largest airports (particularly Heathrow) with others then meeting overspill. Policy should be driven by the best outcomes for passengers, and this should require airports to meet as much local demand as possible. Heathrow is, of course, the closest airport to central London where the largest number of origins and destinations are but channelling demand from other parts of the UK is not necessarily in the best economic interests of the UK.

CILT(UK)’s view is the expansion at any airport should be permitted if there is a positive balance of benefits and costs and provided the airport owner is prepared to invest in expansion. The benefits will be primarily economic, including jobs and trade and the costs will include environmental issues including noise, local air quality and surface access. This is, in effect, the current MBU policy and CILT(UK)’s view is that this should be applied throughout the UK, with each application for expansion determined by the appropriate body (Local Planning Authority, Planning Inspectorate or Secretary of State)

The hub issue

The Airports Commission and the current ANPS argue that the UK needs to maintain Heathrow as a hub. Until 2019, 30-33% of Heathrow’s passengers were connecting. In 2022 to 2024, this figure has dropped to 21-24%. Figures are not available for 2025 and the very recent changes resulting from war in the Gulf are not clear. However, the key point about connecting traffic is that it enables more routes, or higher frequencies, to be provided, thus providing an overall benefit to the UK. If passengers do not connect at Heathrow, they will do so elsewhere, mostly outside the UK. Airlines, particularly home based, so British Airways at Heathrow, have the ability to adjust fares to encourage or discourage connecting passengers and, while this is a very useful measure in the short term, it is not a satisfactory long-term strategy as it is susceptible to factors outside the airline’s control.

British Airways has never operated a demand aggregation system with waves of arrivals and departures, unlike Delta at Atlanta or KLM at Amsterdam. Such hub operations are very costly in both fixed infrastructure and manpower and are not particularly suited to London’s time zone position (which tends to support only one key arrivals/departures peak).

The role of smaller long haul aircraft types is a current factor, with the A321XLR appearing as a challenger to the principle of large wide-bodied aircraft. Some years ago, the B787 was initially hyped as a ‘hub-buster’ and did not really result in many new routes, although it has been a good provider of long-haul leisure services. More regional routes to other hubs have used B777, A330 and even A380s. The A321XLR may find some niche routes but the economics are not obvious. Considering all of the above CILT(UK)’s overall view is that, while there are some benefits in the hub model, they can be added into the balance but are not overwhelming.

...The role of smaller long haul aircraft types is a current factor, with the A321XLR appearing as a challenger to the principle of large wide-bodied aircraft...

Aircraft size

An issue noted above is that greater use of runway capacity can be made with larger aircraft, or higher loads. This is sometimes noted as relating to large aircraft, such as the A380 but, given that many movements are by A320, B737 or similar, trends in these types have more influence on average loads. Passengers per ATM at South East Airports, apart from London City and Southend, are similar (between 158 and 177 in 2025), even though Heathrow has a much larger proportion of larger aircraft.

The generally upward trend in average loads over the last 20 years has been driven by the replacement of smaller versions of the A320 and B737 families by larger types. Most recently, the A321 is replacing A320s and the B737MAX is replacing earlier B737s. There has also been some ‘densification’ in recent years, and load factors have also grown. Wide-bodied aircraft are also being replaced by larger versions, such as the B787-10, B777X and A350-1000.

This trend has been noted in several recent expansion inquiries, Gatwick has forecast 206 passengers per ATM in 2047, Stansted 186 in 2041, and Luton 179 in 2043. For Heathrow, we can note that 200 passengers per ATM on 480,000 movements is 96 million passengers.

Air cargo

The Airports Commission report and the ANPS are deficient in their consideration of air cargo and the DfT does not have a developed air cargo forecasting model. However, our Air freight briefing paper of 2022 provided key insights into this sector.

The ANPS support for the expansion of Heathrow notes that it would provide the greatest benefits (of the shortlisted schemes) for freight, including a doubling of freight capacity. However, there is no analysis of the demand or forecasts. MBU does not mention freight or cargo.

The ANPS should consider elements of the air cargo system in detail, including:

Integrators operate global Hub & Spoke networks and UK is no exception. DHL and UPS have hubs at East Midlands Airport, UPS and FedEx at Stansted. The requirements for this type of operation are night operations (no curfews), fast turnaround of aircraft (<90 minutes), on-site customs, adequate runway length for long-haul freighters and the ability for seamless air to land and land to air access.

Much of the current growth in UK air cargo is driven by eCommerce. Many of the Chinese eCommerce platforms are now taking more responsibility for their own linehaul with operators such as SF Express, flying their own freighters to the UK as well as chartering lift in from Maersk or Air One for example. They still use the integrators for lift but are doing more of the linehaul themselves. This also can provide improved end to end time-in-transit and therefore a service improvement to their customers. The result is that demand is moving away from traditional consolidated freight to time-definite flows and regional distribution models.

UK competitiveness has been negatively impacted by the additional customs protocols that are required versus EU gateways. Customs friction and delays can cause carriers to focus on alternate non-UK airports. Customs performance should therefore be considered as a strategic enabler.

Air cargo requires the integration of planning and development for facilities and surface access. As well as on-airport facilities, associated infrastructure is required, often in locations near airports, plus the necessary road and rail access to enable intermodal distribution throughout the country.

In 2025, Heathrow had by a long way the largest UK tonnage, 96% of which is carried in belly holds. There were 2,380 all-cargo ATMs out of the total of 484,340. In addition, a significant amount, some 40% of the UK’s total. of ‘air’ cargo is carried on trucks to and from other airports, many in mainland Europe via the Channel Tunnel and the Port of Dover. The government should be concerned with the extent of the UK’s reliance on EU airports to handle our cargo and on the potential threats to supply chain security. Truck driver shortages, the reluctance of some EU transport companies to operate to the UK, and the delays at Short Straits Crossings all impact on the speed and cost of transporting UK air cargo to and from the country. Scope for growth will depend on the spare capacity in belly holds, and on the increasing use of larger wide-bodied aircraft such as the A350-1000, B787-10 and B777X. The current ground facilities can be redeveloped to provide increased capacity and surface access for cargo is not a significant constraint. Even without a third runway, tonnage could grow to 2 million tonnes. There is support in the logistics and air cargo sector for a third runway at Heathrow, who argue that Heathrow’s range of flights with belly-hold capacity cannot be replicated or improved by capacity elsewhere. Our argument is that the proportion of air cargo carried on all-cargo flights in the UK is significantly lower than other countries (in the region of 30/70 compared to 50/50 across the world), reflecting the long-running shortage of capacity at Heathrow and therefore the better use of runway capacity elsewhere, in particular at East Midlands Airport, would result in a situation more comparable with other countries.

East Midlands is the second largest UK air cargo airport with 100% of its 383k tonnes carried on all-cargo ATMs, which are 18,591 out of a total of 43,305. The airport is strategically located for activity for the whole of the UK and has few capacity constraints or movement restrictions. It could grow to 600k tonnes by 2035 to 800k by 2045.

Stansted is the third largest air cargo airport with 95% of its 299k tonnes carried on 8,805 all-cargo ATMs. Stansted has a limit of 274,000 total ATMs of which no more than 16,000 can be cargo ATMs. It is likely that, with the passenger growth to 51 million, the total number of ATMs will approach the limit and the number available for all-cargo aircraft will be constrained. While some new long-haul routes will provide opportunities for belly hold cargo, it is considered that growth will be constrained.

The larger regional airports such as Manchester, Edinburgh and Birmingham could see significant growth if they attract more long-haul flights. Manston is assumed to open before 2035 and can accommodate significant tonnages, if cross channel road freight carried as air cargo can be diverted. Doncaster Sheffield is assumed to open before 2035. Some smaller airports such as Bournemouth and Prestwick may see growth from a low base, given that a few all-cargo ATMs can result in significant tonnage.

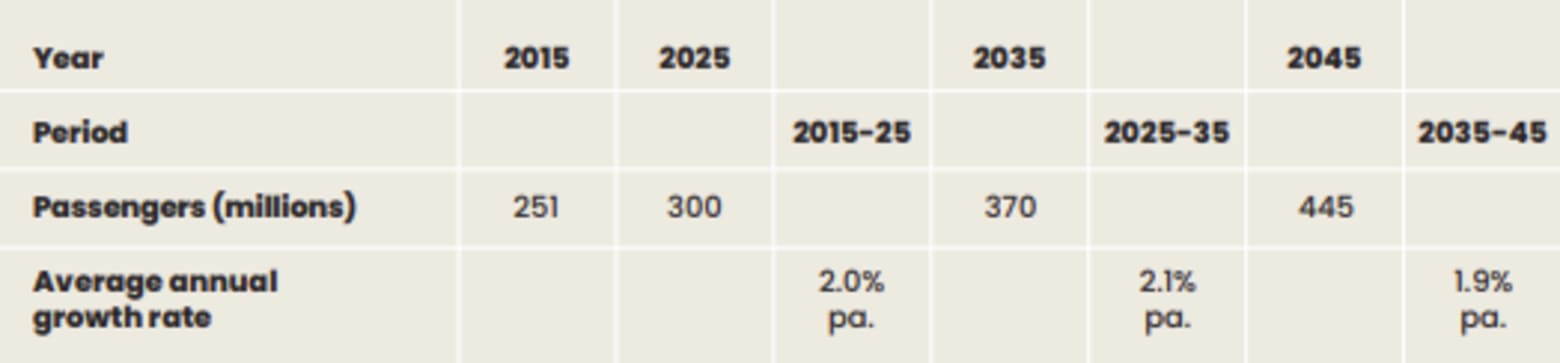

Growth and capacity

If, as we advocate, each airport should make its own case for growth, there need not be a national forecast, other than for the purposes of GHG emissions. However, it is possible to note how a growth rate like the period 2015 to 2025 would result in the following totals (see Table 1).

The 2015 to 2025 period included the Covid period, but numbers had recovered by 2025. We suggest that the propensity to fly, either outbound UK passengers or inbound non-UK visitors will continue to grow but, although a ‘normal’ year might see higher growth, history shows that there are always shocks or downturns which affect the long-term pattern.

...Outside the South East and East of England regions, most airports operate well below their theoretical capacity...

With the approved expansions as noted earlier, there is more than enough capacity to accommodate this growth. Outside the South East and East of England regions, most airports operate well below their theoretical capacity and can accommodate as much traffic as they can attract with relatively modest expansions. Within the South East and East of England, Gatwick at 75 mppa, Stansted at 51 mppa, Luton at 32 mppa, London City at 9 mppa and 5 mppa at smaller airports, plus 90 mppa at Heathrow, gives a total of 262 mppa, which would accommodate growth of 2% pa. for 20 years. These airports would be operating at close to their capacity by 2045, but further expansions could be approved during that period.

Cargo capacity is concentrated on a smaller number of airports as noted earlier, and total UK tonnage could be as follows (see Table 2).

These are perhaps optimistic overall growth rates but there would be ample capacity at the key cargo airports to accommodate this level of growth.

GHG emissions

The Government has asked the Climate Change Committee (CCC) for specific advice in relation to the ANPS review. While this is awaited, it should be noted that the current Government policy is to manage aviation carbon emissions at the national level, which should therefore be a key part of the ANPS. DfT’s aviation forecasting model includes carbon forecasts so should be able to demonstrate how expansion leads to net zero by 2050 using assumptions about measures including operational improvements, new aircraft, sustainable fuel, ETS and CORSIA plus carbon capture. The forecasts can also incorporate the latest knowledge on non-CO2 effects as well as taking account of the Supreme Court’s ruling in the Finch case.

Surface access

CILT (UK) has studied airport surface access in detail and published a report in 2024 and is finalising a report for publication imminently using more recent data. Comments on surface access have also been included in many of CILT(UK)’s submissions or consultation responses about specific airport expansion plans.

The ANPS deals extensively with surface access, in particular relating to the situation with a third runway at Heathrow. The MBU refers only briefly to the subject. Existing airport surface access policy can be summarised from two policy documents as follows:

The 2013 Aviation Policy Framework says “5.12 The general position for existing airports is that developers should pay the costs of upgrading or enhancing road, rail or other transport networks or services where there is a need to cope with additional passengers travelling to and from expanded or growing airports. Where the scheme has a wider range of beneficiaries, the Government will consider, along with other relevant stakeholders, the need for additional public funding on a case-by-case basis.”

The 2025 National Planning Policy Framework (NPPF) says: “116 Development should only be prevented or refused on highways grounds if there would be an unacceptable impact on highway safety, or the residual cumulative impacts on the road network, following mitigation, would be severe, taking into account all reasonable future scenarios."

While the surface access headline is often noted in terms of Public Transport Mode Share (PTMS) for air passengers, the whole picture must include staff travel, cargo and delivery vehicles. CILT(UK)’s latest report seeks to understand catchment areas for air passengers, staff and cargo.

Surface access issues are relevant to some of the capacity assessments for individual airports. While requiring some improvements in surface access, most airports will not be specifically constrained by surface access, except the following:

Gatwick must achieve a 55% PTMS as a condition of its Northern Runway approval. CILT(UK)’s review, as set out in recent published report on Gatwick Rail Access, is that this can be achieved over time by more services at night and on Sundays, increasing the length of trains and by marketing strategies.

The ANPS notes that Heathrow is committed to achieve a 55% PTMS by 2040 with a third runway. The 2024 figure was 41.5%. Some increase should be possible with more mainline rail services and an increased frequency on the Piccadilly line. However, significant growth in PTMS along with a growth in total passengers would require additional rail infrastructure, either the Heathrow Southern Railway (HSR) or the Western Rail Access to Heathrow (WRATH). Either of these would require large capital expenditure and it is not clear how this would be funded, given the APF policy noted above. The ANPS preferred scheme requires the diversion of the M25 as well as extensive road changes elsewhere and this will add significantly to the capital cost, unless the Government is prepared to fund some of the changes.

Luton’s Green Controlled Growth mechanism requires the PTMS to be 45% (2024 29.5%) for growth to continue beyond a specified level.

Birmingham will be linked to HS2 from the early 2030s, and it is not clear what effect this will have, although it should be positive because it will be relatively much closer to London.

Leeds Bradford may be constrained beyond its current capacity unless a new rail station enables a significant shift of travel away from road access

Manchester’s 2024 PTMS was 17.6% but there is no specific limit on expansion related to surface access. Plans for Northern Powerhouse Rail are being developed which include a new station at the Airport, and plans are also being developed to extend the Metro via this new station. Assuming these plans are implemented, there should be no surface access constraint on growth.

Edinburgh’s 2024 PTMS of 40.1% should enable growth in the medium term but, if growth continues in the longer term, further public transport enhancements will probably be needed.

Bristol may struggle to meet the NPPF paragraph 116 test if it cannot increase its PTMS and avoid severe road congestion. In the longer term the WEST rapid transit proposal would enable growth.

...While the surface access headline is often noted in terms of Public Transport Mode Share (PTMS) for air passengers, the whole picture must include staff travel, cargo and delivery vehicles. CILT(UK)’s latest report seeks to understand catchment areas for air passengers, staff and cargo...

Finance

CILT(UK) supports the general principle that, apart from certain special circumstances, the aviation sector should not be publicly funded. Most of the cost of expansion noted above can be met by the owners and operators of the airports (even if they are publicly owned, then on a stand-alone basis). The owners may be overseas investors who are attracted by long term returns related to clear and stable policies. There is a particular issue of funding for surface access, given the policy noted above, but this depends on the individual circumstances of the split of benefits of any surface access improvement between the airport and the wider community. However, the key point is that the passenger and cargo shipper should pay for the operation and expansion of the airport, primarily through air fares and other revenues collected by the airlines, or by retail and other revenues paid by passengers to the airport through concessions etc.

The ANPS notes that, while the Heathrow third runway would be most expensive of the three shortlisted options, it would be financeable without Government support, although it would require the agreement of airlines to pay for it through airport charges. The CAA has considered how to finance expansion as part of its role as economic regulator and has undertaken studies and consultations. The key point is whether expansion should be funded by charges to the airlines in advance of new capacity being available or should it be a project financing arrangement whereby the airport funds the expansion (possibly through borrowing) and then obtains a return from airline charges once capacity is available. Statements made during this period may be part of the negotiating process but it is clear that there are big differences between the parties that may not be possible to be bridged by the CAA. Such concerns are behind the support for an alternative scheme for Heathrow expansion out forward by the Arora group which, although they have been rejected by the Government as the basis for the ANPS review, are still active and may be brought forward alongside any proposals by HAL at the DCO stage.

It is also worth noting HAL’s argument that a third runway will result in more competition which will reduce fares for passengers. Of course, enabling additional airlines to operate and adding competition will, in general, reduce air fares but competition already exists across the UK’s airports and, in the South East and East of England in particular, low cost airlines operate from several airports providing competition for the largest markets in London. At Heathrow there is extensive competition on major routes such as to New York and some low-cost airlines operate (Veuling, Eurowings) but it seems unlikely that a major low-cost airline operation can be established at Heathrow, given the high charges that will be applied.

Heathrow third runway

There are alternative options for the length of a third runway, and we do not express a view about the respective merits. However, we note the option of a phased approach which could enable a proportion of the benefits to be realised early while retaining the option of a full-length runway for later. This would require the safeguarding for the full-length runway to be adopted. Such safeguarding would also be appropriate if the need for additional runway capacity is, as is our view, some way into the future.

Conclusion and summary

CILT(UK)’s view is that:

The ANPS review should cover the whole of the UK and should therefore incorporate the MBU policy.

The expansion at any airport should be permitted if there is a positive balance of benefits and costs and provided the airport owner is prepared to invest in expansion.

While DfT’s aviation forecasts can be a starting point, the revised ANPS should consider scenarios where the need for expansion at individual airports depends on the individual merits of each case.

There is more than enough existing and potential capacity within the UK, and particularly within the South East and East of England, without a third runway at Heathrow for the next twenty years.

However, to be clear, CILT(UK) would support expansion at Heathrow including a third runway if a case can made that the benefits (including the benefits of a hub operation and increased competition) outweigh the costs (including local environmental costs and the appropriate contribution to surface access) and that the airlines and airlines can agree an acceptable funding arrangement, and such expansion should be safeguarded.

Changes in aircraft size will, on the one hand, continue to result in an increase in average loads thus making better use of existing runway capacity. On the other hand, new long haul aircraft types will enable thinner routes to be operated directly without the need to fly via a hub.

The revised ANPS/MBU must include an analysis of and forecast for air cargo, including the role of integrators, trucked air cargo and forecasts, noting the specific requirements of all-cargo aircraft operations.

Surface access may constrain expansion at some airports unless funding solutions are found for infrastructure.

The Climate Change Committee’s advice on aviation expansion should demonstrate how the 2050 net zero commitment will be met.

CILT (UK)

The Chartered Institute of Logistics and Transport in the UK is a professional institution embracing all transport modes whose members are engaged in the provision of transport services for both passengers and freight, the management of logistics and the supply chain, transport planning, government and administration. Our principal concern is that transport policies and procedures should be effective and efficient, based on objective analysis of the issues and practical experience, and that good practice should be widely disseminated and adopted. The Institute has several specialist forums, a nationwide structure of locally based groups and a Public Policies Committee which considers the broad canvass of transport policy.

This submission draws on contributions principally by the Aviation Policy Group.

We plan to engage with national government and local authorities, but we are always interested to hear from or about other interested parties, so if you have any comments on what you have read, please contact the Aviation Policy Group: Daniel Parker-Klein, Director of Policy, Communications and Insight.

Email: policy@ciltuk.org.uk

To download this review, please click here.